DISCOVER THE STACK NOTE™

SAFE vs Convertible Note vs STACK Note

Choosing between a SAFE, a Convertible Note, a KISS note or a Structured venture note (STACK Note™) directly impacts founder dilution, ownership control, governance, and long-term capital strategy.

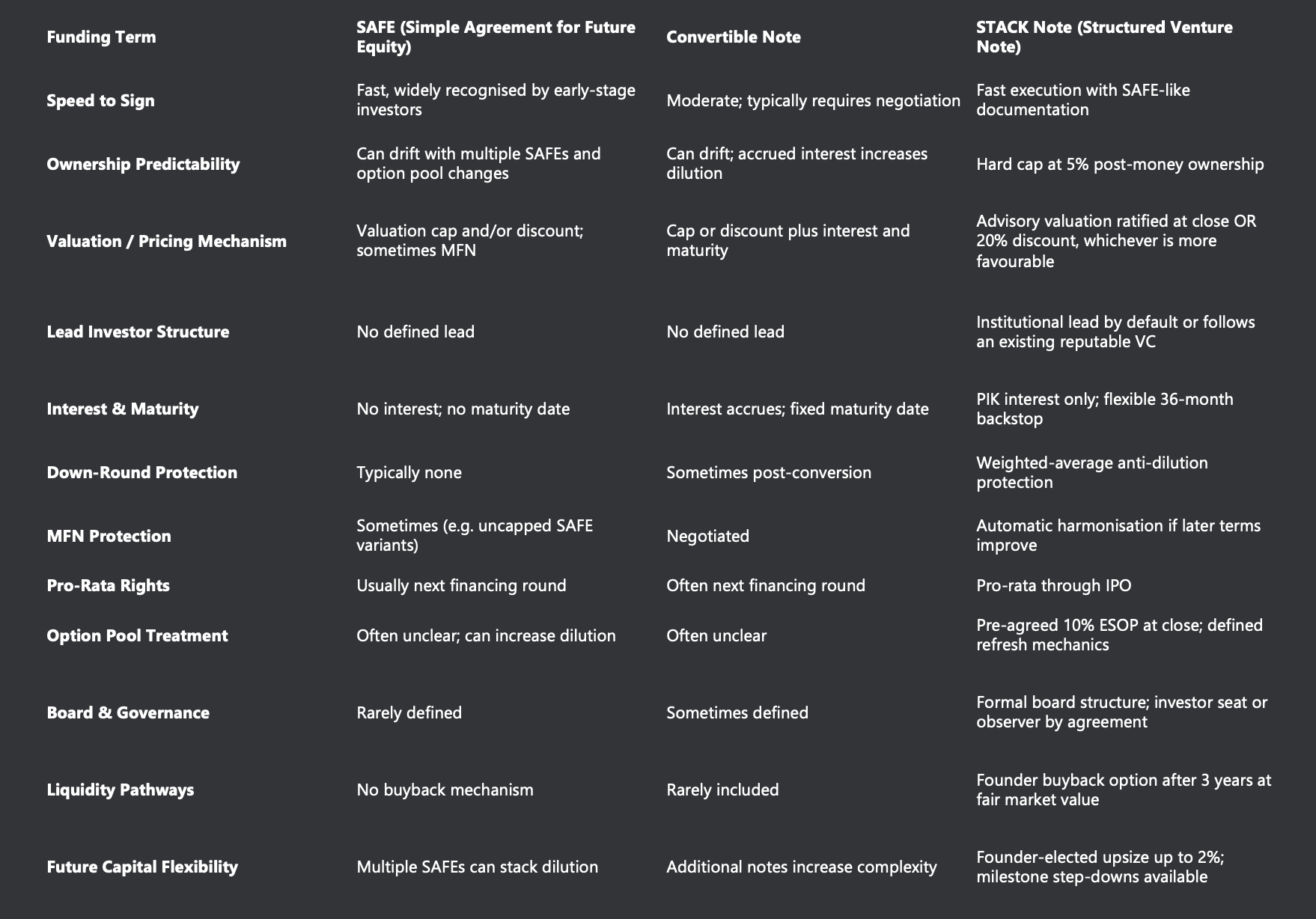

This guide compares the three most common early-stage funding instruments used in pre-seed and seed venture capital. Comparison of startup funding instruments including SAFE, Convertible Notes, and structured venture notes. This table outlines differences in speed to sign, ownership predictability, valuation mechanisms, investor structure, dilution risk, governance, and long-term capital flexibility.

Startup Funding Instrument Comparison Table

SAFE vs Convertible Note: Key Structural Differences

SAFE Agreements

SAFEs are popular in early-stage venture capital due to speed and simplicity. However, they can create ownership drift when multiple SAFEs are issued across pre-seed and seed rounds.

Key risks:

• Dilution stacking

• Option pool surprises

• No maturity discipline

• No formal governance structure

Convertible Notes

Convertible notes introduce interest accrual and a maturity clock. They are debt instruments that convert into equity.

Key structural considerations:

• Interest increases dilution

• Maturity creates repayment pressure

• Negotiation complexity higher than SAFE

• Governance still often undefined

STACK Note: Structured Venture Instrument

The STACK Note is designed to combine speed with ownership clarity and institutional governance.

Structural features include:

• Hard post-money ownership cap

• Defined ESOP treatment

• Formal board formation

• Anti-dilution protection

• Long-term pro-rata alignment

• Defined liquidity and buyback path

This structure is built to reduce founder dilution uncertainty while maintaining investor discipline.

Which Funding Instrument Is Best for Early-Stage Founders?

The answer depends on:

• Desired ownership predictability

• Dilution tolerance

• Governance readiness

• Capital strategy through Series A

• Long-term alignment with investors

For founders raising institutional capital, instrument structure is not cosmetic. It directly affects cap table stability, control rights, and future round dynamics.

## How this tool fits into your capital strategy

Equity instruments define how ownership is structured over time.

To understand how these instruments convert and impact dilution, explore:

These guides explain how financing structures affect long-term ownership.